Import of electricity or natural gas into the EU - obligations under the REMIT

- Category: REMIT

Specific REMIT clause in the contract is needed when company imports electricity or natural gas into the EU.

Green finance disclosures - supervisory expectations during the interim period

- Category: Taxonomy

As most of the provisions on sustainability-related disclosures laid down in the SFDR have started applying from 10 March 2021 and the product-related taxonomy disclosures apply for financial products with respect to the climate change mitigation and climate change adaptation from 1 January 2022, single rulebook on taxonomy disclosures has been established (although on a temporary basis).

It is regrettable that, on account of legislative delays, once more supervisory authorities replace in this role authorised legislative bodies.

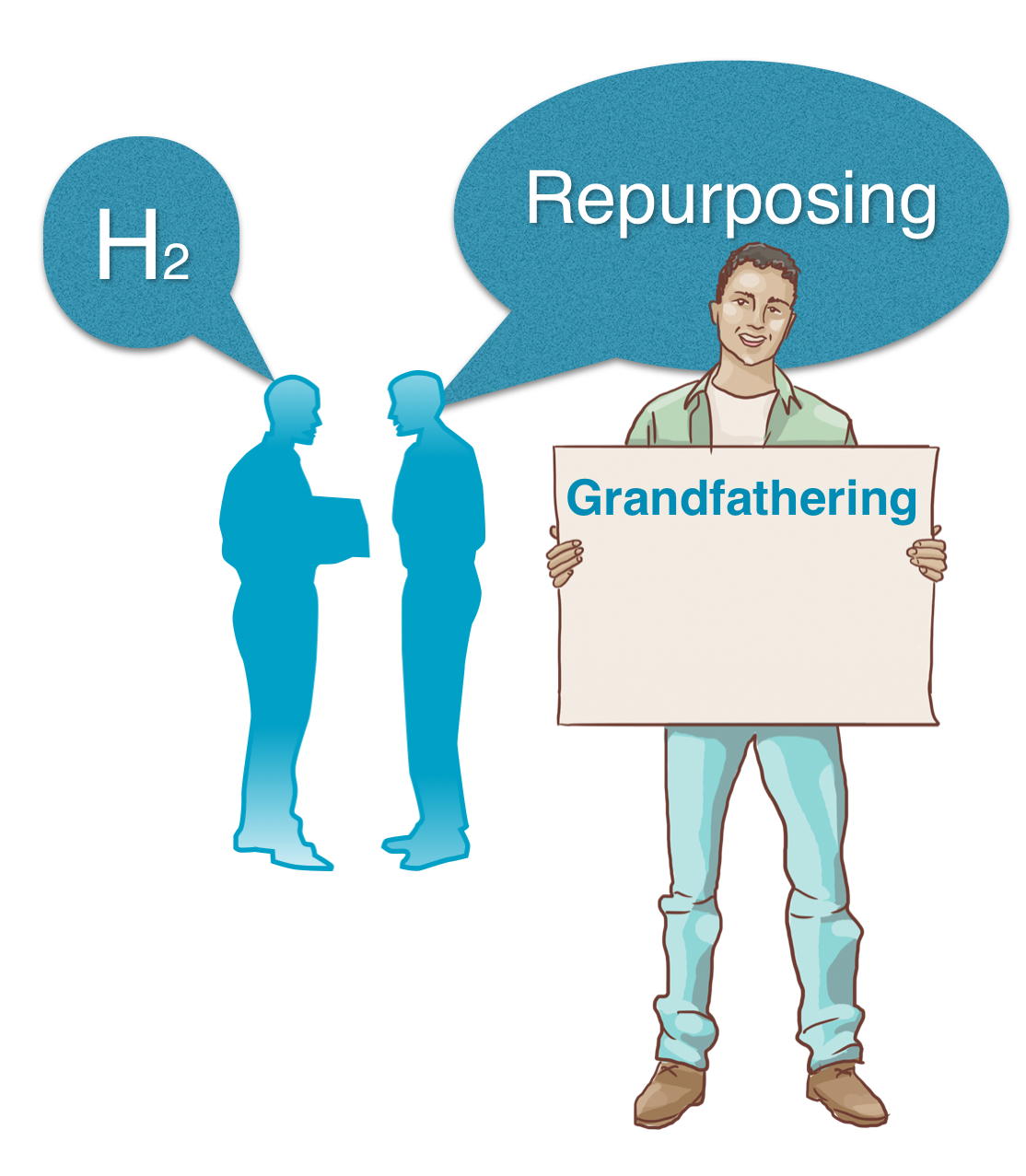

Repurposing of natural gas for hydrogen assets - grandfathering of authorisations

- Category: Hydrogen

Under the new EU draft Directive authorisations granted under national law for the construction and operation of existing natural gas pipelines and other network assets will be grandfathered in the administrative permit granting processes for the deployment of hydrogen production facilities and hydrogen system infrastructure.

Under the new EU draft Directive authorisations granted under national law for the construction and operation of existing natural gas pipelines and other network assets will be grandfathered in the administrative permit granting processes for the deployment of hydrogen production facilities and hydrogen system infrastructure.

According to the draft law conditions for these licences in case of such repurposing must not materially change as compared to natural gas.

MiFID own account exemption modified - but something missing

- Category: Financial Market

European Commission Proposal of 25 November 2021 for a MiFID II amendment removes the licensing requirement for persons dealing on own account on a trading venue by means of direct electronic access (DEA) to the extent that they do not provide or perform any other investment services.

Article 1(2) of the European Commission Proposal of 25 November 2021 for a Directive of the European Parliament and of the Council amending Directive 2014/65/EU on markets in financial instruments (COM(2021) 726 final) modifies Article 2(1), point (d), point (ii) of MiFID II by deleting any references to the DEA.

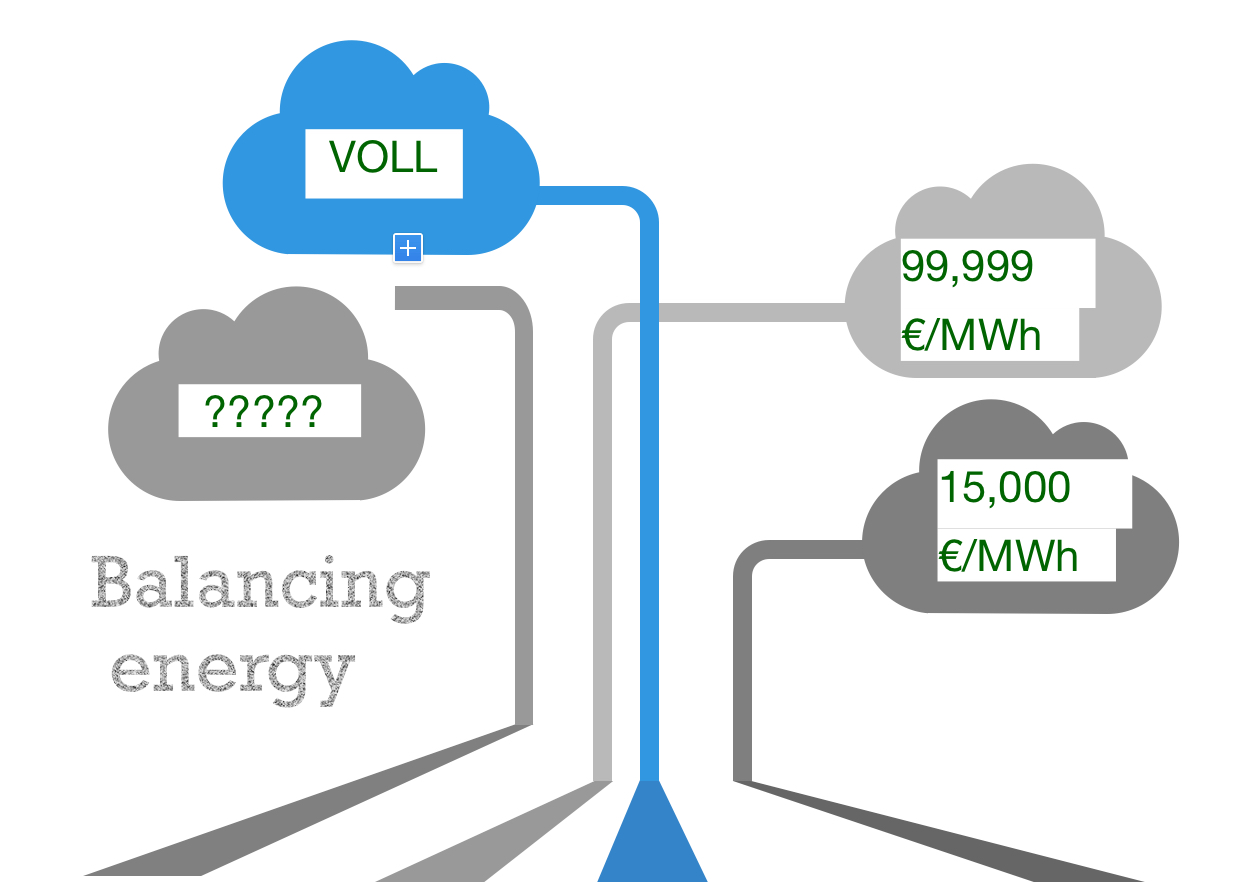

Balancing energy price limit temporarily at 15,000 €/MWh

- Category: Energy market

The importance of balancing energy in the overall electricity market follows from the fact that it is required to ensure electricity system stability under the penalty of the blackout - if it is not available on a sufficiently firm basis.

What should be its price then? Some say that even greater than the VoLL, simply because of obvious collateral damages of the blackout.

Existing technical price limit (99,999 €/MWh) seems to be quite high and the ACER considers it is “sufficiently high”.

Nevertheless, it is transitionally lowered (see ACER Decision No 03/2022 of 25 February 2022 on the amendment to the methodology for pricing balancing energy and cross-zonal capacity used for the exchange of balancing energy or operating the imbalance netting process).

But the word: "limit" is not involved with any restrictions as when it is approached, its value is heightened. So, the sky is the limit?

Partial clearing of the day-ahead electricity market - settlement of FTR Options

- Category: Energy market

The evolution from the physical transmission rights (PTRs) to financial transmission rights (FTRs) in the form of options becomes a dominant feature the European cross-border electricity market.

This inevitably creates opportunities and further supports new forms and models of electricity trading, nevertheless, gives rise to new risks, which market participant must mitigate on its own.

Among these risks is the one involving potential partial clearing of the day-ahead market.

In such case the holders of FTR Options would be compensated in at the day-ahead market spread, which is the difference between the day-ahead price of the neighbouring bidding zone and the day-ahead price of the not cleared bidding zone (currently capped at 3,000€/MWh), while being exposed to the imbalance settlement price in that zone, which can be capped at a price higher than 3,000€/MWh.

Page 2 of 69