REMIT carve-out

The term: "REMIT carve-out" is involved with the new arrangements MiFID II Directive brings to the commodity derivatives market.

|

|

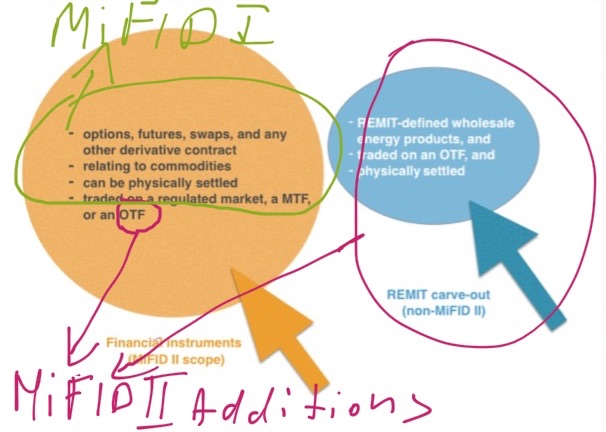

The key MiFID II amendment in that regard is that the scope of financial instruments will include physically-settled derivatives traded on an Organised Trading Facility (OTF).

"REMIT carve-out" represents the plain language description for an exception from the above-mentioned principle and refers to the Regulation No 1227/2011 on the integrity and transparency of the wholesale energy markets.

Thus, "REMIT carve-out" means derivatives with electricity and natural gas as underlying that must be physically settled, which are covered by the REMIT Regulation (wholesale energy products within the REMIT terminology) traded on an OTF, and which do not qualify as MiFID II financial instruments and are consequently outside the scope of MiFID, EMIR and the CRD IV package.

This rule sometimes entails serious consequences, for example, energy contracts covered by the REMIT carve-out do not qualify for netting under the MiFID II positions limits regime, which may cause, in turn, that entities having large such positions will approach the position limit sooner.

In general, products covered with the REMIT carve-out are exempted from MiFID II position limits and position reporting requirements. MiFID II requires of the REMIT carve-out contracts that they "must be physically settled" (MiFID II subordinate legislation specifies what this phrase precisely means).

Reason for such a specific treatment of wholesale energy products covered by REMIT is this particular piece of legislation has its own specific legal framework, which, in the absence of the "REMIT carve-out", could collide with MiFID II rules.

OTF as a platform for trading REMIT carve-out products

It is noteworthy, in the Questions and Answers on MiFID II and MiFIR market structures topics (ESMA70-872942901-38, Question 17 of 3 October 2017) ESMA reserved, that it would not be compliant with MiFID II if an OTF offered trading in C(6) REMIT wholesale energy products only.

To be authorised as an OTF, a multilateral trading system must offer trading in bonds, structured finance products, emission allowances and derivatives, i.e. in financial instruments, without prejudice to the other requirements to be met for such authorisation.

MiFID II Annex I Section C6 Financial instruments

"Options, futures, swaps, and any other derivative contract relating to commodities that can be physically settled provided that they are traded on a regulated market, a MTF, or an OTF, except for wholesale energy products as defined in Article 2 paragraph 4 of Regulation (EU) No 1227/2011 traded on an OTF that must be physically settled"

A trading platform that is authorised as an OTF based on trading financial instruments can, in addition, offer trading in REMIT carve-out” contracts (i.e. in wholesale energy contracts that must be physically settled). ESMA highlighted in this context that “the OTF must ensure that genuine trading in financial instruments takes place on the OTF to be authorised, and retain authorisation, as an OTF, with appropriate staff, IT, financial and other resources being devoted to this activity. Trading in financial instruments should not be designed for the sole purpose of obtaining an OTF license and with the end-objective of trading REMIT carve-out contracts almost exclusively”.

MiFID II/MiFIR provisions applicable to an OTF which trades in REMIT carve-out products

As was said above, REMIT wholesale energy products are not financial instruments, while MiFID II/MiFIR provisions apply, in principle, to the operation of an OTF trading financial instruments.

|

See also:

Physically-settled commodity derivatives under MiFID II

|

Hence, an ambiguity appeared as to the scope of MiFID II/MiFIR provisions applicable to an OTF engaged in trading in REMIT carve-out contracts.

ESMA referred to this issue in the Answer 18 of 3 October 2017 in the Questions and Answers on MiFID II and MiFIR market structures topics (ESMA70-872942901-38).

ESMA requires that a market operator or an investment firm operating an OTF trading both financial instruments and REMIT carve-out products should identify, prevent or otherwise manage any potential adverse consequences that trading in REMIT carve-out products may have on trading in financial instruments and on its ability to meet its MiFIDII/MiFIR obligations on an on-going basis.

Moreover, upon request, the operator of the OTF should be able to explain to the competent authority the procedures and arrangements put in place to that effect.

Where a person seeks authorisation as an OTF and intends to offer trading in REMIT carve-out contracts as well, a detailed description of the REMIT carve-out trading activity should be included in the authorisation file so that the competent authority can understand and assess the potential impact of REMIT carve-out trading on the investment firm or market operator operating the OTF and on trading in financial instruments.

The information to be provided is set out in ITS 19 (Commission Implementing Regulation (EU) 2016/824 of 25 May 2016 laying down implementing technical standards with regard to the content and format of the description of the functioning of multilateral trading facilities and organised trading facilities and the notification to the European Securities and Markets Authority according to Directive 2014/65/EU of the European Parliament and of the Council on markets in financial instruments).

Where an investment firm or market operator operating an OTF has been authorised and intends to additionally offer trading in REMIT carve-out products, a detailed description of the REMIT carve-out trading activity should be provided to the competent authority in due course before the start of such trading activities.

The management body of the investment firm (or the market operator) operating the OTF is responsible for defining, approving and overseeing the organisation of the firm or market operator for the provision of investment services and activities, taking into account the nature, scale and complexity of its business and all the requirements the firm has to comply with.

ESMA is of the view that the responsibilities of the management body extends to the non-financial instrument trading activity of the OTF as they may have an impact on the investment activities provided by the investment firm (or the market operator). This also applies to the management body’s responsibilities governing the investment firm (or market operator)’s internal policy setting out, among other things, the activities, products and operations offered or provided in accordance with risk tolerance of the firm (or the market operator).

Practical examples

For access to the EEX OTF market a separate OTF membership will be required (the same applies for access to the PEGAS market segment of the Powernext OTF).

Additionally, the preconditions for the EEX OTF membership are:

- the admission to the regulated market of EEX,

- a valid balancing agreement with the relevant transmission system operator (TSO) or agreements with third parties providing access thereto.

The latter condition is also present on OTF at Powernext for trading on non-financial instruments only (Customer information of 27 October 2017, EEX, Pegas, “EEX and Powernext Non-MTFs markets to be replaced by Organized Trading Facilities (OTF) in line with MiFID II”).

The reference to the “valid balancing agreement with the relevant transmission system operator” in the above EEX and Pegas Customer information represents a clear allusion to Article 5(1)(a) of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing Directive 2014/65/EU of the European Parliament and of the Council as regards organisational requirements and operating conditions for investment firms and defined terms for the purposes of that Directive.

The said provision stipulates the conditions that the product must fulfil to be considered a “wholesale energy products that must be physically settled” (destined for REMIT carve-out trading).

It says that for the purposes of Section C(6) of Annex I to Directive 2014/65/EU, a wholesale energy product must be physically settled where, among other things, “it contains provisions which ensure that parties to the contract have proportionate arrangements in place to be able to make or take delivery of the underlying commodity; a balancing agreement with the Transmission System Operator in the area of electricity and gas shall be considered a proportionate arrangement where the parties to the agreement have to ensure physical delivery of electricity or gas.”

Another interesting information in the above EEX and Pegas customer information of 27 October 2017 is that:

- the OTF products and the corresponding exchange-traded products share the same settlement prices.

- margin requirements in OTF products and the respective corresponding exchange-traded products will be netted.

Heterogeneity of the MiFID II Section C6

It needs to be further observed (as underlined by ESMA on 19 December 2016 in Answer 2 in the Questions and Answers on MiFID II and MiFIR commodity derivatives topics, ESMA70-872942901-28), the Section C6 of the MiFID II covers three differentiated groups of contracts, the products within the REMIT carve-out being only one of them.

Remaining two categories include:

- C6 energy derivatives contracts (those with coal or oil as underlying traded on an OTF that must be physically settled), and

- the rest of C6 instruments.

C6 energy derivatives contracts benefit from the second exception to the indicated MiFID II rule for inclusion of physically-settled derivatives traded on an OTF into the scope of financial instruments, subject, however, to different conditions.

Impact of Brexit

The ESMA Public Statement of 7 October 2019 (Impact of no-deal Brexit on the application of MiFID II/MiFIR and the Benchmark Regulation (BMR), ESMA70-155-8500) deals with possible implications of a no-deal Brexit for the functioning of a REMIT carve-out mechanism.

The starting point is that under the REMIT provisions, the following contracts are considered to be wholesale energy products (save for the specificity of final customers):

- contracts for the supply of electricity or natural gas where delivery is in the EU,contracts for the supply of electricity or natural gas where delivery is in the EU;

- derivatives relating to electricity or natural gas produced, traded or delivered in the EU; and

- derivatives relating to the transportation of electricity or natural gas in the EU, irrespective of where those derivatives are traded.

As a consequence, a derivative contract related to electricity or natural gas that would be exclusively produced, traded and delivered in the UK would no longer qualify as wholesale energy product post-Brexit and would no longer be eligible to the C(6) carve-out under MiFID II, even if traded on an EU27 OTF. However, where, for instance, UK natural gas would continue to be traded on a spot trading platform in the EU27 post-Brexit, derivatives on UK natural gas would continue to qualify as “wholesale energy products” under Article 2(4) of REMIT and could benefit from the C(6) carve-out in MiFID II. Further, to be eligible to the REMIT carve-out, the wholesale energy product must be traded on an OTF. Accordingly, where a wholesale energy product would not be traded on an EU27 OTF post-Brexit, it would cease to be eligible to the C(6) carve-out under MiFID II.

ESMA in the above document concludes that:

- where a derivative contract based on electricity or natural gas would no longer be eligible to the C(6) carve-out under MiFID, it may become a financial instrument under Section C(6) if traded on an EU regulated market or multilateral trading facility or traded on an EU OTF without meeting the REMIT definition;

- derivative contract no longer eligible to the C(6) carve-out may also become a financial instrument under Section C(7) of Annex I of MiFID II if, among other things, it has the “characteristics of other derivative financial instruments” as further defined in Article 7 of Commission Delegated Regulation 2017/565.

Also in the Notice of 13 July 2020 to Stakeholders on Withdrawal of the United Kingdom and EU rules in the field of markets in financial instruments (REV1 - replacing the notice dated 8 February 2018) the European Commission observed that in the absence of the relevant agreement, where a wholesale energy product would not be traded on an EU OTF, it would cease to be eligible to the C(6) carve-out under MiFID II.

REMIT carve-out extinguished?

The ESMA in the Consultation Paper of 5 November 2019 “MiFID II review report on position limits and position management, Draft Technical Advice on weekly position reports” (ESMA70-156-148) expressed an opinion that the REMIT carve-out mechanism should be reconsidered, as it is “the source of a major competitive disadvantage for regulated markets and MTFs, which ESMA can find no justification for” and it “penalises the already more heavily regulated trading venues”.

Moreover, “ESMA considers that the same rules should apply to the same instruments independently of the EU trading venues where those instruments are traded and that the logic for any such differentiation remains unclear”.

However, the Council of European Energy Regulators (CEER) in its response of 20 December 2019 (Ref: C19-MIT-84-03) did not agree with ESMA’s analysis that the C (6) carve-out creates an unlevel playing field across trading venues. CEER’s stance is that the REMIT carve-out should not be reconsidered in a restrictive way.

In support of its stance the CEER invoked the following arguments:

- considering, the main business of energy companies is the production and/or supply of electricity or gas, energy companies use derivatives as a way of hedging (managing production and supply risks) and do not pose a systemic risk to the financial system nor do they pose any risk to private investors - these circumstances have not changed from previous years and from the previous regulatory framework,

- gas and electricity markets have their own dedicated regulation to address market abuse and transparency – the REMIT Regulation, which has the main goal to bring more integrity and transparency (analogously as MiFID II does in financial markets),

- REMIT foresees that each national regulatory authority has the investigatory and enforcement powers necessary to exercise the prohibitions against market abuse (article 13).

Finally, in the document of 1 April 2020 "MiFID II Review report on position limits and position management" (ESMA70-156-2311, p. 24) ESMA withdrew its initial proposition.

ESMA Consultation Paper of 5 November 2019 “MiFID II review report on position limits and position management, Draft Technical Advice on weekly position reports” (ESMA70-156-148)

5.1.2 Reconsider the C(6) carve-out exemption

88. ESMA shares the concerns expressed by some respondents with regard to the shift of trading in physically-settled wholesale energy contracts (REMIT contracts) from regulated markets and MTFs to OTFs post-MiFID II as a result of the C(6) carve-out and the unlevel playing field this exemption has created.

89. Indeed, under the current framework, the exact same REMIT contract is subject to different rules, depending on where it is traded. Instruments traded on regulated markets and MTFs are subject to position limits as well as to other applicable MiFID II/MiFIR requirements, while identical instruments traded on OTFs are not considered as financial instruments and fall outside the scope of any of these obligations.

90. Unsurprisingly, the C(6) carve-out has proved a significant and successful incentive for market participants to move trading in REMIT contracts to OTFs and is the source of a major competitive disadvantage for regulated markets and MTFs, which ESMA can find no justification for.

91. ESMA first notes that the creation of the OTF category aimed at making the EU financial markets more transparent and efficient and at levelling the playing field between various venues offering multilateral trading services8. In ESMA’s view, the C(6) carve-out does not achieve this objective as it deliberately creates a competitive advantage for OTFs trading REMIT products. Furthermore, ESMA notes that the C(6) carve-out penalises the already more heavily regulated trading venues. More fundamentally, ESMA considers that the same rules should apply to the same instruments independently of the EU trading venues where those instruments are traded and that the logic for any such differentiation remains unclear.

92. Consequently, ESMA is of the view that the current rules allowing for the exemption of the wholesale energy products traded on OTFs should be reconsidered.

Questions and Answers on MiFID II and MiFIR commodity derivatives topics, ESMA70-872942901-28

Ancillary activity

Question 2 [Last update: 19/12/2016]

Does trading activity in C6 contracts which takes place on OTFs after 3 January 2018 need to be counted towards the ancillary thresholds prior to that date?

Answer 2

We differentiate between wholesale energy products categorised as C6 within the REMIT scope (derivatives with electricity and natural gas as underlying traded on an OTF that must be physically settled), C6 energy derivatives contracts (those with coal or oil as underlying traded on an OTF that must be physically settled) and the rest of C6 instruments.

Financial instruments under MiFID I which will also be financial instruments within C6 under MiFID II should count towards the trading activity and assessed against the ancillary thresholds.

C6 with coal or oil as underlying and the rest of C6 instruments count throughout the calculation period to determine market size, as OTC instruments until January 3, 2018 and as OTF on-venue instruments after that. For C6 instruments with coal or oil as underlying traded on OTFs this assessment is based on them only being exempted from certain EMIR obligations for a transitional period while they are being classified as financial instruments throughout the period. The same applies to the computation of positions by non-financial corporates.

Questions and Answers on MiFID II and MiFIR market structures topics, ESMA70-872942901-38

Question 17 [Last update: 03/10/2017]

Can an OTF offer trading in C(6) REMIT wholesale energy products only?

Answer 17

No. Under Article 4(1)(23) of MiFID II, an organised trading facility (OTF) is a multilateral trading system which organises the interaction of multiple third party buying and selling interests in bonds, structured finance products, emission allowances and derivatives, i.e. in financial instruments.

Accordingly, to be authorised as an OTF, a multilateral trading system must offer trading in the financial instruments listed above, without prejudice to the other requirements to be met for such authorisation. However, a trading platform that is authorised as an OTF based on trading financial instruments can, in addition, offer trading in wholesale energy contracts that must be physically settled ( “REMIT carve-out” contracts).

ESMA highlights that the OTF must ensure that genuine trading in financial instruments takes place on the OTF to be authorised, and retain authorisation, as an OTF, with appropriate staff, IT, financial and other resources being devoted to this activity. Trading in financial instruments should not be designed for the sole purpose of obtaining an OTF license and with the end-objective of trading REMIT carve-out contracts almost exclusively.

Question 18 [Last update: 03/10/2017]

When an OTF authorised to trade financial instruments also trades REMIT wholesale energy products, i.e. in non-financial instruments, what are the applicable MiFID II/MiFIR provisions?

Answer 18

MiFID II/MiFIR provisions apply to the operation of an OTF trading financial instruments. Where a person seeks authorisation as an OTF and intends to offer trading in REMIT carve-out contracts as well, a detailed description of the REMIT carve-out trading activity should be included in the authorisation file so that the competent authority can understand and assess the potential impact of REMIT carve-out trading on the investment firm or market operator operating the OTF and on trading in financial instruments. The information to be provided is set out in ITS 19 (Commission Implementing Regulation (EU) 2016/824 of 25 May 2016 laying down implementing technical standards with regard to the content and format of the description of the functioning of multilateral trading facilities and organised trading facilities and the notification to the European Securities and Markets Authority according to Directive 2014/65/EU of the European Parliament and of the Council on markets in financial instruments).

Where an investment firm or market operator operating an OTF has been authorised and intends to additionally offer trading in REMIT carve-out products, a detailed description of the REMIT carve-out trading activity should be provided to the competent authority in due course before the start of such trading activities.

The management body of the investment firm (or the market operator) operating the OTF is responsible for defining, approving and overseeing the organisation of the firm or market operator for the provision of investment services and activities, taking into account the nature, scale and complexity of its business and all the requirements the firm has to comply with. ESMA is of the view that the responsibilities of the management body extends to the non-financial instrument trading activity of the OTF as they may have an impact on the investment activities provided by the investment firm (or the market operator). This also applies to the management body’s responsibilities governing the investment firm (or market operator)’s internal policy setting out, among other things, the activities, products and operations offered or provided in accordance with risk tolerance of the firm (or the market operator).

More generally, ESMA highlights that a market operator or an investment firm operating an OTF trading both financial instruments and REMIT carve-out products should identify, prevent or otherwise manage any potential adverse consequences that trading in REMIT carve-out products may have on trading in financial instruments and on its ability to meet its MiFIDII/MiFIR obligations on an on-going basis. Upon request, the operator of the OTF should be able to explain to the competent authority the procedures and arrangements put in place to that effect.